Last Updated: February 2026 | Written by a property investor with 8+ years of experience in Southeast Asian markets

Whether you’re a first-time overseas investor or looking to diversify your portfolio, this article answers the real questions people ask about Philippine real estate investment.

What Makes the Philippines Attractive for Property Investment?

Let’s start with the basics. Why should you even consider the Philippines when places like Vietnam or Thailand get more attention?

Strong Economic Fundamentals

The Philippine economy has been one of Southeast Asia’s consistent performers. According to the World Bank, the country’s GDP grew by 5.6% in 2023 and is projected to maintain growth between 5.8-6.2% through 2025.

Here’s what drives that growth:

- Young population: Median age is just 25.7 years. That means a growing workforce and increasing demand for housing.

- BPO industry: The Philippines is the world’s second-largest call center hub, employing over 1.57 million people.

- Remittances: Overseas Filipino Workers (OFWs) send home roughly $36 billion annually, much of which flows into property purchases.

- Rising middle class: An estimated 8 million households now qualify as middle-income earners.

These aren’t abstract statistics. They translate directly into rental demand and property appreciation.

Affordable Entry Points Compared to Regional Markets

Let me put this in perspective with actual numbers:

| City | Prime Area Price/sqm | Average Rental Yield |

|---|---|---|

| Singapore | $15,000 – $25,000 | 2.5% – 3.5% |

| Hong Kong | $20,000 – $35,000 | 2.0% – 2.8% |

| Bangkok | $4,500 – $8,000 | 4.0% – 5.5% |

| Manila (BGC/Makati) | $3,500 – $6,000 | 6.0% – 8.5% |

| Cebu City | $2,000 – $3,500 | 7.0% – 10.0% |

The math is straightforward. Lower entry costs plus higher yields equals better returns on investment. A studio unit in BGC might cost you $80,000-$120,000. The same money buys you a parking spot in Singapore.

Can Foreigners Buy Property in the Philippines? 🏠

This is probably the most common question I get. The short answer: yes, with restrictions.

What Foreigners CAN Buy

- Condominium units: Foreigners can own up to 40% of a condominium project’s total units. This is the most popular option for overseas investors.

- Buildings (but not land): You can own the structure itself.

What Foreigners CANNOT Buy Directly

- Land: The Philippine Constitution restricts land ownership to Filipino citizens and corporations with at least 60% Filipino ownership.

- Houses on freehold land: Since the house sits on land you can’t own, this creates complications.

Legal Workarounds for Land Ownership

Many foreign investors use these legitimate structures:

- Long-term lease: You can lease land for up to 50 years, renewable for another 25 years. Total: 75 years.

- Corporation structure: Form a Philippine corporation with 60% Filipino and 40% foreign ownership. The corporation can then own land.

- Spouse ownership: If married to a Filipino citizen, the property can be registered under their name.

I personally went with a condominium for simplicity. The legal framework under the Condominium Act (RA 4726) is clear and well-established.

Pro tip: Always work with a lawyer who specializes in real estate transactions. Budget around PHP 30,000-50,000 ($540-$900 USD) for legal fees. It’s money well spent.

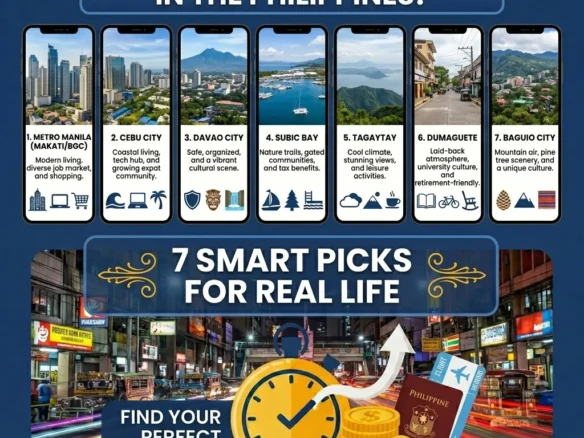

Where Should You Invest? Best Locations in the Philippines for Real Estate

Location matters more than anything else. I’ve seen identical units in the same city have completely different rental performance based on their exact location.

Metro Manila: The Economic Powerhouse

Bonifacio Global City (BGC)

This is where I bought my first property. BGC is essentially Manila’s version of Singapore—clean streets, modern infrastructure, lots of expats and professionals. Rental demand stays strong because multinational companies have offices here.

- Average price: PHP 200,000-350,000 per sqm ($3,600-$6,300 USD)

- Rental yield: 5-7% gross

- Best for: Professionals, expats, long-term appreciation

Makati CBD

The original financial district. Older buildings but established infrastructure. Rockwell Center and Legaspi Village remain premium addresses.

- Average price: PHP 180,000-300,000 per sqm

- Rental yield: 5-8% gross

- Best for: Business travelers, corporate rentals

Ortigas Center

More affordable than BGC or Makati. Home to several BPO companies. Good rental demand from young professionals.

- Average price: PHP 120,000-180,000 per sqm

- Rental yield: 6-9% gross

- Best for: Budget-conscious investors seeking yield

Cebu City: The Queen City of the South

Cebu has surprised many investors. The IT Park and Cebu Business Park have created strong demand for residential units. Plus, tourism drives short-term rental income.

- Average price: PHP 100,000-180,000 per sqm

- Rental yield: 7-10% gross

- Best for: Higher yields, tourism-linked income

Davao City: The Emerging Market

President Duterte’s hometown saw significant infrastructure investment. It’s still early-stage compared to Manila or Cebu, which means lower prices and potentially higher appreciation.

- Average price: PHP 80,000-140,000 per sqm

- Rental yield: 6-8% gross

- Best for: Long-term investors comfortable with less liquidity

| Location | Entry Price (Studio) | Gross Yield | Liquidity | Growth Potential |

|---|---|---|---|---|

| BGC, Manila | $90,000+ | 5-7% | High | Moderate |

| Makati CBD | $85,000+ | 5-8% | High | Moderate |

| Ortigas | $55,000+ | 6-9% | Medium | Good |

| Cebu IT Park | $50,000+ | 7-10% | Medium | Good |

| Davao City | $40,000+ | 6-8% | Low | High |

How Much Does It Really Cost to Buy Property in the Philippines?

The sticker price is just the beginning. Here’s a realistic breakdown of what you’ll actually pay.

Purchase Costs Breakdown

| Cost Item | Percentage/Amount | Who Typically Pays |

|---|---|---|

| Documentary Stamp Tax (DST) | 1.5% of selling price or zonal value (whichever is higher) | Buyer |

| Transfer Tax | 0.5-0.75% (varies by city) | Buyer |

| Registration Fee | ~0.25% (based on sliding scale) | Buyer |

| Notarial Fee | 1-2% (negotiable) | Buyer |

| Capital Gains Tax | 6% of selling price or zonal value | Seller (sometimes negotiated) |

| Agent Commission | 3-5% | Seller |

| Legal Fees | PHP 30,000-100,000 | Buyer |

Rule of thumb: Budget an additional 5-8% on top of the purchase price for transaction costs.

Ongoing Costs to Consider

- Association dues: PHP 50-150 per sqm monthly for condos

- Real Property Tax (RPT): 1-2% of assessed value annually

- Property management: 8-12% of monthly rent if you hire a manager

- Rental income tax: 25% for non-residents (can be reduced via tax treaties)

What Are the Risks of Investing in Philippine Real Estate?

I’d be doing you a disservice if I only talked about the upside. Here’s what can go wrong—and how to protect yourself.

Risk #1: Developer Delays or Bankruptcy

Pre-selling (buying off-plan) is common in the Philippines. You might pay for 3-4 years before getting your unit. Sometimes developers delay. Occasionally, they fail entirely.

Mitigation:

- Stick with established developers: Ayala Land, SM Development Corporation (SMDC), Megaworld, DMCI Homes

- Check the developer’s track record with DHSUD (formerly HLURB)

- Verify the License to Sell before paying anything

Risk #2: Currency Fluctuation

The Philippine peso can be volatile. In 2022, it weakened significantly against the US dollar. This cuts both ways—good for dollar-based buyers purchasing, bad when repatriating rental income.

Mitigation:

- Consider peso-denominated loans if rates are favorable

- Factor in currency hedging costs for large investments

- Take a long-term view (5+ years minimum)

Risk #3: Oversupply in Certain Areas

Some locations have too many units chasing too few tenants. The Bay Area in Manila, for instance, has seen vacancy rates climb due to aggressive development.

Mitigation:

- Research vacancy rates before buying

- Focus on locations with diverse demand drivers (not just residential speculation)

- Talk to actual property managers about rental realities

Risk #4: Natural Disasters

The Philippines experiences typhoons, earthquakes, and flooding. This is a reality you need to accept.

Mitigation:

- Check flood maps before purchasing (Metro Manila Flood Map available from PAGASA)

- Choose buildings with modern construction standards

- Get comprehensive property insurance

Step-by-Step: How to Buy a Condo in the Philippines as a Foreigner

Here’s the actual process I followed. It’s more straightforward than you might expect.

Step 1: Find Your Property

Browse listings on:

- Lamudi – largest property portal

- Property24

- Developer websites directly

- Licensed brokers (verify with PRC)

Step 2: Reservation and Due Diligence

- Pay reservation fee (typically PHP 20,000-50,000 for condos)

- Verify the Condominium Certificate of Title (CCT) with the Registry of Deeds

- Confirm the 40% foreign ownership cap hasn’t been reached

- Review the Master Deed and Declaration of Restrictions

Step 3: Contract to Sell

You’ll sign a Contract to Sell outlining:

- Payment terms (spot cash, installment, or bank financing)

- Turnover date

- Penalties for default

Step 4: Payment

Options include:

- Spot cash: Usually gets you 5-15% discount

- Installment: Common for pre-selling (no interest during construction period)

- Bank financing: Possible but difficult for non-residents

Step 5: Deed of Absolute Sale and Transfer

- Execute the Deed of Absolute Sale

- Pay Documentary Stamp Tax at the Bureau of Internal Revenue (BIR)

- Pay Transfer Tax at the local treasurer’s office

- Register with the Registry of Deeds

- Receive your CCT

Timeline: For ready-for-occupancy (RFO) units, expect 30-60 days from reservation to title transfer. Pre-selling takes 3-5 years until turnover.

Tax Implications for Foreign Property Investors in the Philippines

Nobody likes taxes, but understanding them prevents nasty surprises.

Rental Income Tax

Non-resident foreigners pay a flat 25% withholding tax on gross rental income. If your country has a tax treaty with the Philippines, you might qualify for reduced rates or credits.

Countries with tax treaties include: USA, UK, Australia, Canada, Japan, South Korea, and most EU nations. Check the BIR’s list of tax treaties.

Capital Gains Tax on Sale

When selling, you’ll pay 6% Capital Gains Tax based on the selling price or zonal value (whichever is higher). This applies regardless of whether you actually made a profit.

Estate and Inheritance

Philippine properties are subject to 6% estate tax upon the owner’s death. Consider how this factors into your estate planning.

What’s the Future Outlook for Philippine Real Estate? 📈

I’m cautiously optimistic. Here’s why:

Positive Indicators

- Infrastructure spending: The “Build Better More” program continues major projects including Metro Manila Subway, NLEX-SLEX Connector, and New Manila International Airport

- POGO exodus creating opportunity: As online gaming operators leave, quality units are returning to the rental market at more reasonable prices

- Tourism recovery: 2024 saw over 5 million tourist arrivals, supporting short-term rental demand

- Demographic dividend: The population will keep growing until at least 2050

Concerns to Watch

- Interest rates remain elevated by historical standards

- Oversupply in certain submarkets

- Political and regulatory uncertainty

My take: Focus on prime locations with genuine demand drivers. Avoid speculative projects in fringe areas. And always buy for cash flow, not just appreciation.

Checklist: Before You Buy Philippine Property ✅

| ☐ | Verify developer’s License to Sell with DHSUD |

| ☐ | Confirm foreign ownership quota not exceeded (40% limit) |

| ☐ | Review Condominium Certificate of Title (CCT) |

| ☐ | Check for liens, encumbrances, or adverse claims |

| ☐ | Verify real property tax payments are current |

| ☐ | Review Master Deed and association rules |

| ☐ | Inspect the actual unit (or have someone inspect for you) |

| ☐ | Research comparable prices in the area |

| ☐ | Talk to existing tenants or owners in the building |

| ☐ | Engage a qualified real estate lawyer |

| ☐ | Understand all transaction costs (budget 5-8% extra) |

| ☐ | Plan for property management if investing remotely |

Frequently Asked Questions About Philippine Real Estate Investment

Is Philippine real estate a good investment in 2025?

For investors seeking 6-10% gross rental yields with potential appreciation, the Philippines offers compelling value compared to regional alternatives. The combination of economic growth, young population, and relatively affordable prices creates favorable conditions. However, success depends heavily on location selection and due diligence.

How much money do I need to start investing in Philippine property?

You can enter the market with approximately $40,000-$50,000 USD for a studio unit in secondary locations like Ortigas or Cebu. Prime areas like BGC require $90,000+ USD. Always add 5-8% for transaction costs.

Can I get a mortgage in the Philippines as a foreigner?

Technically possible but practically difficult. Most banks require Philippine residency or significant local banking history. Many foreign investors pay cash or arrange financing in their home country.

What happens to my property if I pass away?

Philippine succession laws apply. Your property will be subject to 6% estate tax. Consider creating a will under Philippine law and consulting an estate planning attorney.

Sources & References

- World Bank – Philippines Economic Overview

- Philippine Statistics Authority (PSA)

- Bangko Sentral ng Pilipinas – Central Bank

- Bureau of Internal Revenue – Tax Information

- DHSUD (Department of Human Settlements and Urban Development)

- Republic Act 4726 – The Condominium Act

- Colliers Philippines – Market Research

- JLL Philippines – Property Market Reports

- Global Property Guide – Philippines

Final Thoughts

The Philippines won’t make you rich overnight. But for patient investors willing to do proper research, it offers genuine opportunity. Strong yields. Growing economy. Favorable demographics.

Start small if you’re nervous. A single studio unit in a good location teaches you more than any guide ever could. I learned more from my first tenant dispute than from a hundred articles.

Feel free to reach out if you have specific questions. I’m happy to share what I’ve learned—including the mistakes.

Good luck, and happy investing. 🏢

Join The Discussion